Drive Lease Accounting ROI with Managed Services

Learn the value of managed services and how to use it to manage people, processes, and technology.

Strategies for Managing Real Estate Leases

Learn how your organization can reduce your total real estate portfolio spend while automating lease accounting requirements

Achieve Lease Accounting ROI

Understand how a service provider can help manage people, technology, and processes

Lease vs. Buy Analysis

Corporate finance organizations should think about equipment finance and leasing as a strategic tool for the business. In addition to optimizing the use of capital, managing leasing programs proactively can help manage liabilities and improve financial stewardship.

2023 Global Lease Accounting Survey Results

Guidelines for organizations at all stages of adoption, with recommendations for leading practices to make lease accounting more efficient, delivering increased ROI and long-term compliance.

The Real Estate Leader’s Quick Guide

Get actionable insights on market shifts that are changing lease administration.

Project Plan – FASB Lease Accounting Standard

To implement the new lease accounting standards, first you will need to define the project team, gain executive sponsorship…

Healthcare Organization Case Study

Streamlining lease accounting with managed services and implementing real estate lease administration.

Tyson Foods Lease Accounting Case Study

Achieving greater visibility into the lease portfolio.

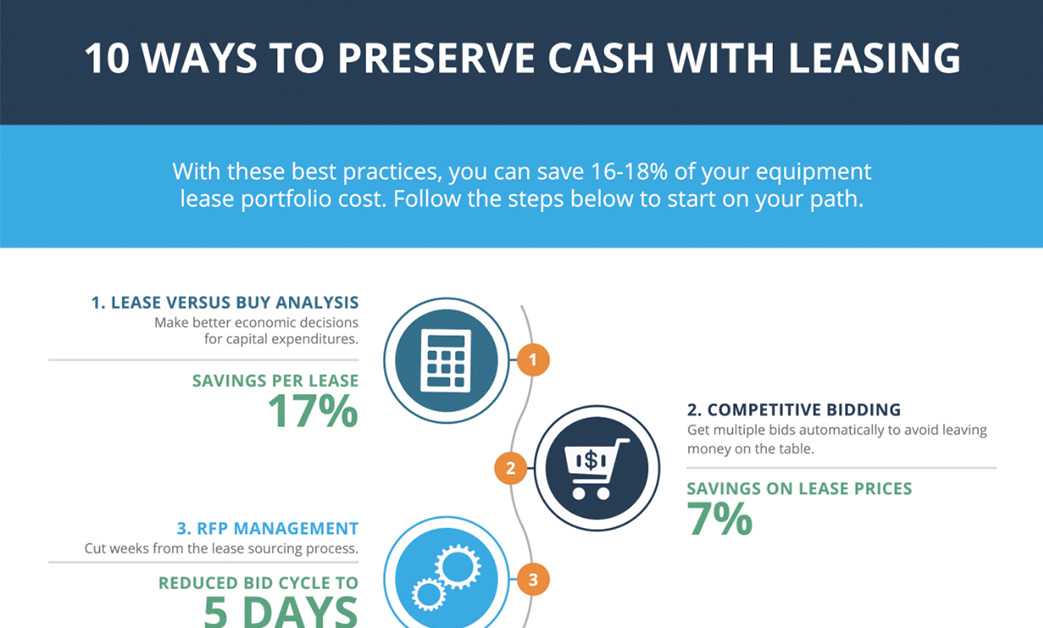

10 Ways to Preserve Cash With Leasing

Looking for ways to preserve cash? Here are 10 ways leasing can help.