“LeaseAccelerator saves us thousands of hours per year.”

"LeaseAccelerator has the ability to handle our complex leases."

"LeaseAccelerator gives us greater visibility of our lease portfolio."

“LeaseAccelerator is helping me save time by saving all leases on one system and generating accurate reports.”

“My favorite part of LeaseAccelerator is the speed of processing leases and the easy-to-use bulk import feature.”

“LeaseAccelerator has saved us COUNTLESS hours of work on a monthly basis.”

“LeaseAccelerator has been a very reliable tool for managing finance and operating lease accounting.”

eBook

9 Ways to Save with Real Estate Lease Administration

Learn ways to reduce costs and errors across your real estate lease portfolio using better processes and automation.

eBook

2023 Global Lease Accounting Survey

Our survey uncovered critical ways to optimize lease accounting.

eBook

Automating the Lease Accounting Monthly Close

Take out cost and risk from the monthly close process with automation.

Video

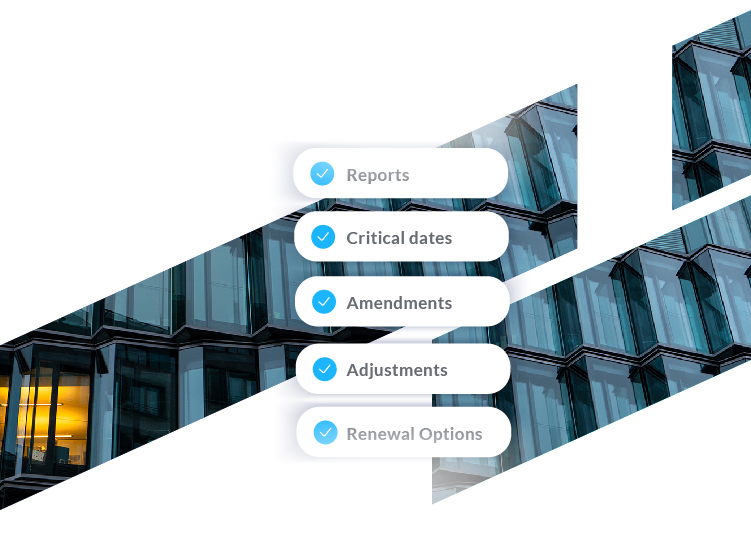

Real Estate Lease Administration Tour

Manage real estate leases and lease accounting in one centralized system.

eBook

Lease vs. Buy Analysis

Get best practices for equipment leasing programs with this PureLease guide.

Offer

Run a Sourcing Event

Have a question, need a quote, or want help finding the right partner? Send us your contact info.