Lease Accounting’s Role in Executing Financial Strategy | Qualified

Learn best practices, hear real-world examples and opportunities to improve the lease lifecycle

Beyond Lease Accounting Compliance – Top Process Changes | Qualified

Learn how organizations are going beyond compliance to achieve growth.

Real Estate Lease Admin | Best Practices | SIOR

Learn how to reduce total real estate spending while automating the lease accounting requirements

Real Estate Lease Admin | Best Practices | Globe St

Learn how to reduce total real estate spending while automating the lease accounting requirements

Real Estate Lease Admin | Best Practices | Connect CRE

Learn how to reduce total real estate spending while automating the lease accounting requirements

Real Estate Lease Admin | Best Practices | Accenture

Learn how to reduce total real estate spending while automating the lease accounting requirements

Real Estate Lease Admin | Best Practices | Qualified

Learn how to reduce total real estate spending while automating the lease accounting requirements

Optimizing Your Equipment Leasing Process | SmartBrief

Learn best practices for using equipment leasing as a strategic tool during economic downturns and beyond

Optimizing Your Equipment Leasing Process | PM

Learn best practices for using equipment leasing as a strategic tool during economic downturns and beyond

Optimizing Your Equipment Leasing Process | Qualified

Learn best practices for using equipment leasing as a strategic tool during economic downturns and beyond

Webinar Registration Template (New) – No Form

Webinar Webinar Title Thursday 22 June 20231:00pm ET | 12:00pm CT | 10:00am PTCredit: 1 CPE Register now In recent years, the commercial real estate (CRE) market has gone through dramatic change, forcing tenants and landlords to reinvent their cost structures and rethink their 3-5 year plans. This reevaluation often includes evaluating workplace utilization, considering […]

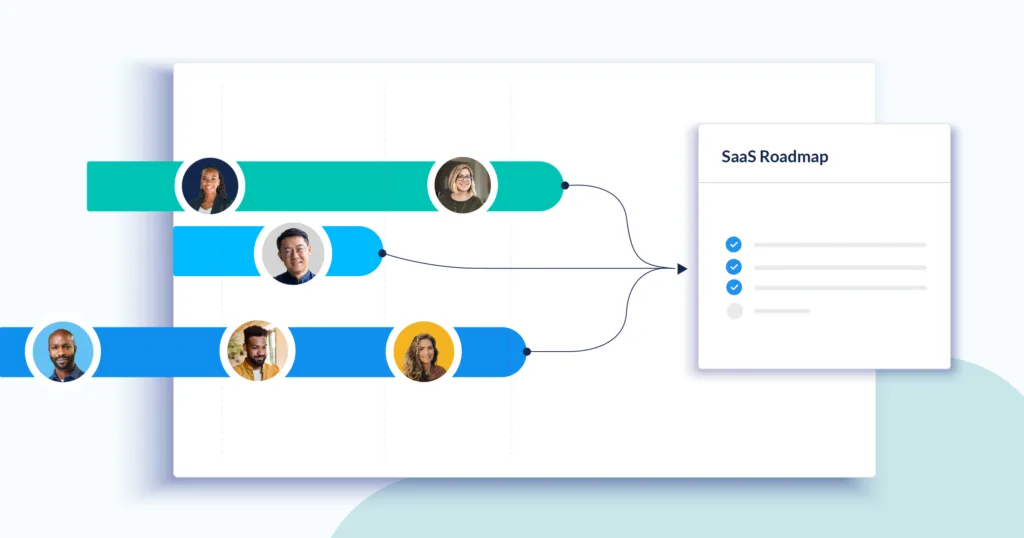

Listening to Clients to Build a SaaS Roadmap

SaaS applications, like the emergence of public cloud computing, enable organizations to focus on where you want to create unique value. That’s what LeaseAccelerator does today too. And, SaaS makes it easy to leverage third-party components to give our clients the best experience.

Getting Lease Accounting Audits Right! | Qualified

Lease accounting specialists will do a deep dive into the elements of a successful, repeatable lease accounting audit

Getting Lease Accounting Audits Right! | BT

Lease accounting specialists will do a deep dive into the elements of a successful, repeatable lease accounting audit

Webinar Registration Template (New)

Webinar Webinar Title Thursday 22 June 20231:00pm ET | 12:00pm CT | 10:00am PTCredit: 1 CPE In recent years, the commercial real estate (CRE) market has gone through dramatic change, forcing tenants and landlords to reinvent their cost structures and rethink their 3-5 year plans. This reevaluation often includes evaluating workplace utilization, considering technology consolidation, […]

Equipment Lease Sourcing Success Stories | Procurement Mag

Learn how competitive sourcing can connect into your overall lease management strategy

Equipment Lease Sourcing Success Stories | Leasing Life

Learn how competitive sourcing can connect into your overall lease management strategy

Equipment Lease Sourcing Success Stories | Qualified

Learn how competitive sourcing can connect into your overall lease management strategy

CRE Trends – Expert Panel | Mohr

Real estate industry leaders review the current market trends and what the future holds for corporate real estate

CRE Trends – Expert Panel | CBRE

Real estate industry leaders review the current market trends and what the future holds for corporate real estate

CRE Trends – Expert Panel | Connect CRE

Real estate industry leaders review the current market trends and what the future holds for corporate real estate

CRE Trends – Expert Panel | Globe Street

Real estate industry leaders review the current market trends and what the future holds for corporate real estate

CRE Trends – Expert Panel | Qualified

Real estate industry leaders review the current market trends and what the future holds for corporate real estate

Lease vs. Buy and Lease Accounting | Best Practices | Qualified

Learn lease versus buy best practices and the financial and strategic benefits to leasing equipment

Expert Panel: The Future of Lease Accounting in 2024 | RGP

Lease accounting experts review lessons learned in 2023 and outline what they expect lease administration and lease accounting to look like in 2024

Real Estate Lease Administration – 10 Ways to Save | Connect CRE

Lease administration experts share how your organization can manage real estate leases effectively

Lease Accounting | Moving Off Spreadsheets | Qualified

Learn to overcome the challenges of spreadsheets and the value of Lease Lifecycle Automation

Real Estate Lease Administration – 10 Ways to Save | CoreNet

Lease administration experts share how your organization can manage real estate leases effectively

Real Estate Lease Administration – 10 Ways to Save | Qualified

Lease administration experts share how your organization can manage real estate leases effectively

Real Estate Lease Administration – 10 Ways to Save | REBO

Lease administration experts share how your organization can manage real estate leases effectively

Lease Accounting ROI: Navigating Through Change | Industry Dive

Learn how your organization can adjust staffing, tools, and process to weather this economic change

Driving ROI with CRE Consolidations | Qualified

Learn practical steps you can implement now to achieve cost savings, better cash flow, and greater collaboration.

9 Ways to Save with Real Estate Lease Administration | LinkedIn (v3)

eBook 9 Ways to Save with Real Estate Lease Administration Commercial real estate leases are complex and expensive — learn ways to find cost savings, including: Centralizing teams Updating lease administration software Managing critical dates Automating processes At most companies, real estate still represents the largest asset category of the leasing portfolio. In addition, the […]

Automating the Lease Accounting Close | LinkedIn v2

Learn ways to reduce cost and risk by automating key elements of your monthly close process.

Real Estate Lease Administration – 10 Ways to Save | Globe St

LeaseAccelerator and Mohr Partners share how your organization can manage real estate leases effectively

Lease Accounting: What Your Auditor Wants to See | LinkedIn

Learn how the right information and lease accounting tools can make your audit easier.

Lease Accounting: What Your Auditor Wants to See | Qualified

Learn how the right information and lease accounting tools can make your audit easier.

Strategies for Managing Real Estate Leases

Learn how your organization can reduce your total real estate portfolio spend while automating lease accounting requirements.

9 Ways to Save with Real Estate Lease Administration | LinkedIn (v2)

eBook 9 Ways to Save with Real Estate Lease Administration Download eBook Commercial real estate leases are complex and expensive — learn ways to find cost savings, including: Centralizing teams Updating lease administration software Managing critical dates Automating processes At most companies, real estate still represents the largest asset category of the leasing portfolio. In […]

10 Cash Preservation Lease Accounting Tactics | TR

Learn how your organization can implement and benefit from strategic leasing decisions to increase cash flow

Optimizing Your Equipment Leasing Process | PM

Learn best practices for using equipment leasing as a strategic tool during economic downturns and beyond

Optimizing Your Equipment Leasing Process | SM

Learn best practices for using equipment leasing as a strategic tool during economic downturns and beyond

Corporate Overview Brochure

Brochure LeaseAccelerator Company Overview Download now The first business application suite for the entire lease lifecycle Lease sourcing Lease administration Lease accounting Lifecycle automation LeaseAccelerator is the leader in enterprise Lease Lifecycle Automation, a new category of financial software that fundamentally reinvents the way that businesses lease. With our software, companies can digitize their leasing […]

Nine Lessons Private Companies Can Learn from Public Companies | LinkedIn (New)

Find out the lessons public companies learned during their lease accounting projects so you can avoid the same mistakes.

Lease Accounting for Private Companies: A Guide to the First 90 Days | LinkedIn (New)

Learn how to identify lease accounting implementation challenges, assess existing processes, and find all of your leases.

Alison Engel Joins LeaseAccelerator as Chief Financial Officer

1/26/2023 – LeaseAccelerator announces today that Alison Engel (Ali) has joined the company as its new Chief Financial Officer (CFO).

Lease Accounting Software Evaluation Guide | LinkedIn

Identify the critical lease accounting software requirements for day 1 compliance and long-term success with ASC 842 & IFRS 16.

9 Ways to Save with Real Estate Lease Administration | LinkedIn

eBook 9 Ways to Save with Real Estate Lease Administration Download eBook Commercial real estate leases are complex and expensive — learn ways to find cost savings, including: Centralizing teams Updating lease administration software Managing critical dates Automating processes At most companies, real estate still represents the largest asset category of the leasing portfolio. In […]

9 Ways to Save with Real Estate Lease Administration | Google

eBook 9 Ways to Save with Real Estate Lease Administration Download eBook Commercial real estate leases are complex and expensive — learn ways to find cost savings, including: Centralizing teams Updating lease administration software Managing critical dates Automating processes At most companies, real estate still represents the largest asset category of the leasing portfolio. In […]

9 Ways to Save with Real Estate Lease Administration | Triblio

eBook 9 Ways to Save with Real Estate Lease Administration Download eBook Commercial real estate leases are complex and expensive — learn ways to find cost savings, including: Centralizing teams Updating lease administration software Managing critical dates Automating processes At most companies, real estate still represents the largest asset category of the leasing portfolio. In […]

Lease Accounting Audit Prep: Closing Out Your Year | LinkedIn

Learn the elements of a successful lease accounting audit in 2023 and beyond

Myths and Risks of Using Spreadsheets for Lease Accounting | LinkedIn Ads

Excel is a great tool for data analysis and decision support but its danger is brought front-and-center when it’s used to manage processes like accounting.

Automating the Lease Accounting Close | LinkedIn

Learn ways to reduce cost and risk by automating key elements of your monthly close process.

Automating the Lease Accounting Close | Google

Learn ways to reduce cost and risk by automating key elements of your monthly close process.

Enhancing Lease Accounting with Managed Services | Qualified

Lease accounting experts from EZLease and PwC discuss the power of managed services

Enhancing Lease Accounting with Managed Services | PwC

Lease accounting experts from EZLease and PwC discuss the power of managed services

Automating the Lease Accounting Close | RGP

Lease accounting experts share practical steps and best practices for automating the close process

Automating the Lease Accounting Close | Qualified

Lease accounting experts share practical steps and best practices for automating the close process

Lease Accounting: Planning for Ongoing Compliance | Scribcor

Learn why organizations need to invest in people, processes, and technology to maintain ongoing compliance

Recalibrating Real Estate Leases

WEBINAR REPLAY: Recalibrating Real Estate Leases Hidden Opportunities to Bolster Cash Flow Recently in the Wall Street Journal, Mike Zechmeister, CFO of C.H. Robinson, was quoted as saying “As we look forward without knowing exactly where this is headed… liquidity is the number one question that rises to the top of the list in terms […]

ASC 842 and GASB 87 – Top Three Challenges of Compliance | Qualified

Webinar ASC 842 and GASB 87 – Top Three Challenges of Compliance Wednesday 17 November 2021 2:00pm ET | 1:00pm CT | 11:00am PT 1 CPE Attendees will learn: The FASB and GASB requirements of the expanded lease definition Understanding data collection and extraction Achieving compliance on the transition date and beyond Ongoing lease accounting […]

Handbook – IASB IFRS 16 Lease Accounting Standard

Handbook ASC 842 Lease Accounting Standard Handbook Get ahead of the FASB ASC 842 lease accounting deadlines while driving savings today. Download handbook to learn: How to get started now Summary of the new FASB ASC 842 rules SEC reporting impacts Data and documents you’ll need to collect Required lease accounting software changes Real world […]

LeaseAccelerator releases major update

9/15/2021 – LeaseAccelerator releases major update to its leading Lease Lifecycle Automation platform with exciting new accounting and reporting enhancements.

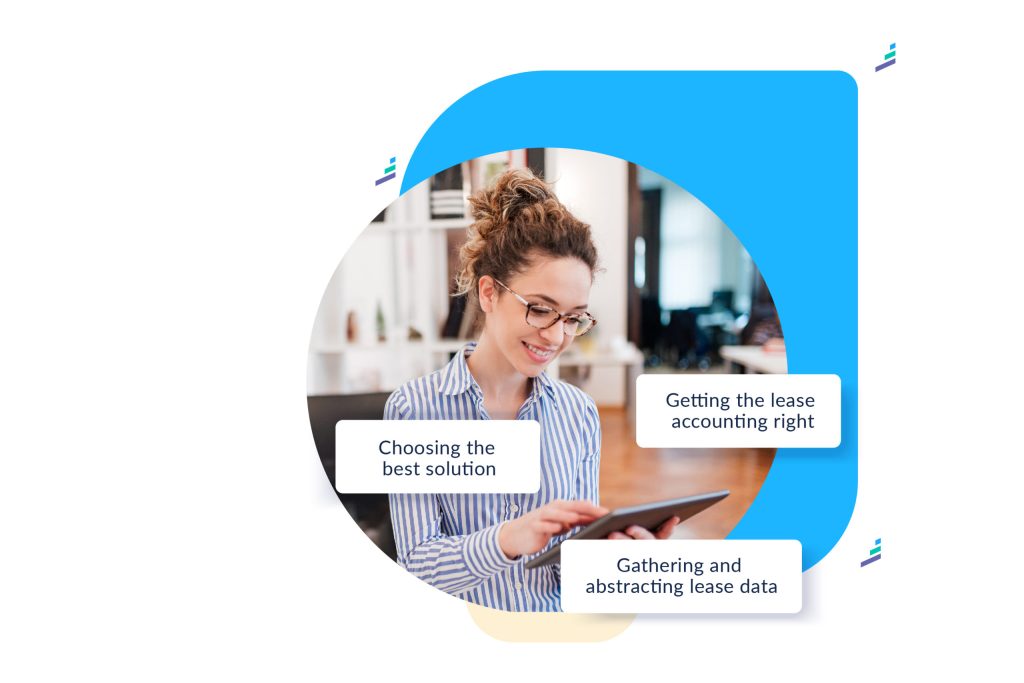

Download FASB & Lease Abstraction | Whitepaper

Whitepaper download FASB & Lease Abstraction Download the whitepaper Ready to take the next step? Get a demo or reach out. Get demo Contact sales

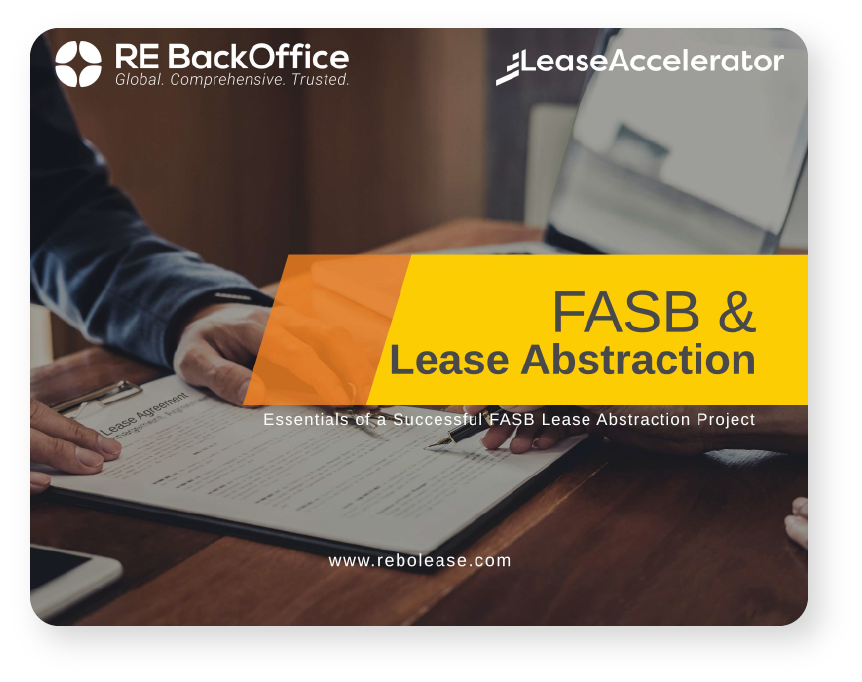

FASB & Lease Abstraction – no form

Whitepaper FASB & Lease Abstraction Get lease data right the first time Taking a systematic approach to lease abstraction right from the beginning will help you build a lease repository that is accurate and relevant and strengthen the foundation of your lease portfolio management process. Download this whitepaper to learn more about how to […]

FASB & Lease Abstraction – REBO promo

Whitepaper FASB & Lease Abstraction Get lease data right the first time Taking a systematic approach to lease abstraction right from the beginning will help you build a lease repository that is accurate and relevant and strengthen the foundation of your lease portfolio management process. Download this whitepaper to learn more about how to […]

Maximising the return on your IFRS 16 investment

Webinar Excelling beyond IFRS 16: A practical guide to moving off spreadsheets to manage lease accounting Thursday 15 April 2021 11am AEST – Sydney, Australia | 1pm NAST – Auckland, New Zealand Duration: 1 Hour In partnership with Deloitte Attendees will learn: Overview of IFRS 16 and the compliance journey Review the linkage between a […]

Partners | Register a LeaseAccelerator Deal

Register a LeaseAccelerator deal Help your clients move beyond spreadsheets. LeaseAccelerator complements your advisory and implementation services, so you can provide more value and better outcomes. Register your deal here and Bryan Seck (VP Global Alliances) will follow up. Register your deal

Lease Accounting for Private Companies: A guide to the first 90 days – Controller’s Council 3-25-21

eBook Lease accounting for private companies: A controller’s guide to the first 90 days of the project Download eBook to: Understand the biggest technical accounting challenges Assess your existing systems, processes, and controls Take an enterprise-wide census of your leases Learn the answers to key questions including: Who to include on the project team How […]

[Old] Cummins Case Study

Cummins achieves benefits by centralizing Equipment Lease Management using standardized processes, controls, and systems.

Lease Accounting Demo – Easier IFRS 16 Compliance

Webinar Lease Accounting Demo Easier IFRS 16 Compliance Wednesday 21 July 2021 10am – Singapore | 12pm – Sydney, Australia | 2pm – Auckland, New Zealand Duration: 45 Mins Attendees will learn: How easy EZLease is to set-up, enabling organisations to move off spreadsheets in less than a day How simple it is to configure […]

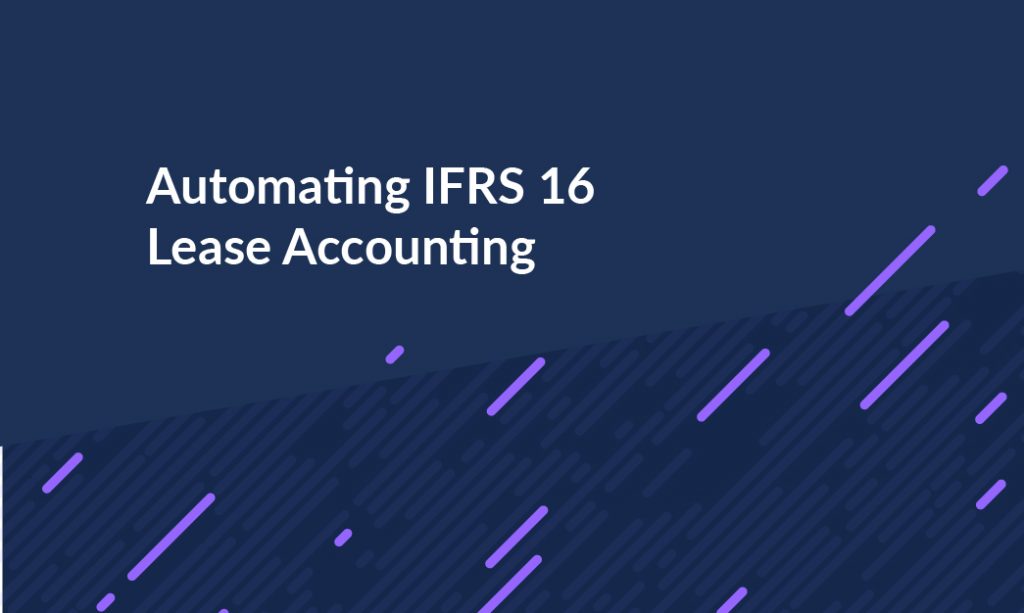

Automating IFRS 16 lease accounting

Listen to leasing experts from Deloitte and LeaseAccelerator to hear practical examples of how to build a business case to automate IFRS 16 lease accounting

Automating IFRS 16 Lease Accounting – Key Considerations When Building a Business Case

Webinar Automating IFRS 16 lease accounting: Key considerations when building a business case Wednesday 16 June 2021 11am AEST – Sydney, Australia | 1pm NAST – Auckland, New Zealand Duration: 45 Mins In partnership with Deloitte Attendees will learn: Overview of the long-term challenges expected when using spreadsheets to comply with IFRS16 Explore the key […]

ASC 842 Workshop – Argyle promotion

Webinar ASC 842 Workshop: Compliance and implementation best practices Tuesday 17 August 2021 2:00pm ET | 1:00pm CT | 11:00am PT | Duration: 1.5 Hours CPE: 1.6 credits Attendees will learn: Uncover the challenges of the new ASC 842 accounting close Get practical steps to kickstart your compliance with ASC 842 Learn best practices from […]

Handbook | ASC 842 Lease Accounting Standard | Form

Handbook ASC 842 Lease Accounting Standard Handbook Get ahead of the FASB ASC 842 lease accounting deadlines while driving savings today. Download handbook to learn: How to get started now Summary of the new FASB ASC 842 rules SEC reporting impacts Data and documents you’ll need to collect Required lease accounting software changes Real world […]

Maximising the return on your IFRS 16 investment

Webinar Maximising the return on your IFRS 16 investment: Using the benefit of hindsight to optimise your future leasing strategy Thursday 27 May 2021 Sydney, Australia – AEST 11am | Auckland, New Zealand – NAST 1pm Attendees will learn: What is Lease Lifecycle Management How the key requirements for choosing an IFRS16 solution has changed […]

ASC 842 Workshop

Webinar ASC 842 Workshop: Compliance and implementation best practices Tuesday 17 August 2021 2:00pm ET | 1:00pm CT | 11:00am PT | Duration: 1.5 Hours CPE: 1.6 credits Attendees will learn: Uncover the challenges of the new ASC 842 accounting close Get practical steps to kickstart your compliance with ASC 842 Learn best practices from […]

Customer Training Center Of Excellence Event EMEA

LeaseAccelerator EMEA Customer Training Event: Center of Excellence Virtual, Instructor-Led Training (VILT) May 17th – 20th, 2021 1:00 pm – 3:00 pm CET Duration: 2 Hours each day 10.8 total CPE credits available Register Now We’re excited to offer a Virtual Instructor-Led Center of Excellence event, which takes place May 17th-20th. Join these daily 2-hour […]

GASB 87: Lease Accounting Data Collection

Learn why data collection is a critical requirement for ensuring successful adoption of the new GASB 87 lease accounting standards and how to identify which data needs to be collected and where to find it.

2021 Global Lease Accounting Survey Report – CFO Dive

Report 2021 Global Lease Accounting Survey Results Learn how your organization compares against the survey benchmarks Get detailed lease accounting research with insights from US public, private and international companies, including: Where they are in their compliance journey Ongoing audit challenges Technology adoption vs. manual processes How lease accounting and other systems are integrated How […]

Excelling beyond IFRS 16: A practical guide to moving off spreadsheets to manage lease accounting – Deloitte

Webinar Excelling beyond IFRS 16: A practical guide to moving off spreadsheets to manage lease accounting Thursday 15 April 2021 11am AEST – Sydney, Australia | 1pm NAST – Auckland, New Zealand Duration: 1 Hour In partnership with Deloitte Attendees will learn: Overview of IFRS 16 and the compliance journey Review the linkage between a […]

Achieve ASC 842 Compliance with Limited Resources

LeaseAccelerator and Baker Tilly cover how private organizations like yours can achieve ASC 842 compliance despite limited resources.

Excelling beyond IFRS 16: A practical guide to moving off spreadsheets to manage lease accounting

Listen to experts from Deloitte, CBRE and LeaseAccelerator as they review the IFRS 16 lease accounting journey thus far and delve into the practicalities of implementing an alternative solution to spreadsheets.

GASB 87 Compliance: It’s Time to Get Ready!

Webinar Replay GASB 87 Compliance: It’s Time to Get Ready! Capture and comply Viewers will learn: What key data elements are required from every lease, and what conditional data elements may also be required Which leases you need to gather data from in order to meet initial compliance and retrospective disclosure requirements How to gather […]

Download Global Lease Accounting Survey

Report download Global Lease Accounting Survey Download the report Ready to take the next step? Get a demo or reach out. Get demo Contact sales

2021 Global Lease Accounting Survey Report

Leverage the survey’s benchmarks and maturity model to help you compare and identify improvements to your leasing process.

EY and LeaseAccelerator Global Lease Accounting Survey – Controller’s Guide eblast

Webinar EY and LeaseAccelerator Global Lease Accounting Survey Results Thursday 18 March 2021 11:00am ET | 10:00am CT | 8:00am PT | Duration: 1 Hour CPE: 1 CPE credit Register now Attendees will learn: Identify opportunities for organizations of all sizes to improve the leasing process Share ways to eliminate cost and risk from lease […]

Excelling beyond IFRS 16: A practical guide to moving off spreadsheets to manage lease accounting

Webinar Excelling beyond IFRS 16: A practical guide to moving off spreadsheets to manage lease accounting Thursday 15 April 2021 11am AEST – Sydney, Australia | 1pm NAST – Auckland, New Zealand Duration: 1 Hour In partnership with Deloitte Attendees will learn: Overview of IFRS 16 and the compliance journey Review the linkage between a […]

EY and LeaseAccelerator Global Lease Accounting Survey – CFO Dive eblast

Webinar EY and LeaseAccelerator Global LeaseAccounting Survey Results Thursday 18 March 2021 11:00am ET | 10:00am CT | 8:00am PT | Duration: 1 Hour CPE: 1 CPE credit Register now Attendees will learn: Identify opportunities for organizations of all sizes to improve the leasing process Share ways to eliminate cost and risk from lease accounting […]

Customer Connect – Full Session – February 2021

LeaseAccelerator Customer Connect February 2021 Agenda: 0:00 – Welcome: Mike Lees, CMO, LeaseAccelerator 2:15 – The Customer Journey: Michael Keeler, CEO, LeaseAccelerator 30:50 – Hewlett Packard’s Customer Journey: Veronica Campos, Finance Manager, HP 55:25 – Hain Celestial’s Migration Story: Ameet Kumar, Global Corporate Controller, Hain Celestial 1:19:55 – Dow Chemical’s Center of Excellence: Scott Boetefuer, […]

Hewlett Packard Case Study

Hewlett Packard Automates Lease Accounting with LeaseAccelerator Lease accounting transformation Veronica Campos, Finance Manager at Hewlett Packard Inc., shares their lease accounting journey with LeaseAccelerator as part of HP’s global transformation. She walks through their current leasing portfolio and the compliance challenges they have overcome with their monthly lease accounting close process. Campos originally shared […]

Dow Chemical Case Study

Dow Chemical Achieves ASC 842 and IFRS 16 Compliance Dow Chemical achieves global compliance with LeaseAccelerator Scott Boetefuer, Finance Director of External Reporting, and Taylor Punches, Team Lead of Lease Accounting at Dow Chemical share their lease accounting journey and how they built a center of excellence with LeaseAccelerator. Dow selected LeaseAccelerator in 2017 when […]

Hain Celestial Case Study

Hain Celestial Migrates Lease Accounting to LeaseAccelerator Global migration and implementation success Ameet Kumar, Global Corporate Controller at Hain Celestial shares their evaluation process, selection criteria, and migration story from KPMG’s KLT to LeaseAccelerator. Hear how quickly Hain Celestial got up and running with a full migration and implementation to achieve sustainable lease accounting compliance, […]

Carnival Case Study

Carnival achieves Audit Readiness with LeaseAccelerator Achieving audit readiness with lease accounting software Diana McDonough, Corporate Accounting Director, Carnival Corporation & plc, shares Carnival’s monthly lease accounting routine and how they achieve audit readiness with LeaseAccelerator. McDonough originally shared this presentation on LeaseAccelerator’s Customer Connect virtual event. Carnival’s lease accounting journey Ready to take the […]

Protected: Webinar Template 2021 Copy

There is no excerpt because this is a protected post.

Lease Accounting for Private Companies: A guide to the first 90 days – AICPA March 2021

eBook Lease accounting for private companies: A guide to the first 90 days of the project Download eBook to: Understand the biggest technical accounting challenges Assess your existing systems, processes, and controls Take an enterprise-wide census of your leases Learn the answers to key questions including: Who to include on the project team How […]

Customer Training Center Of Excellence Event

LeaseAccelerator Customer Training Event: REM Center of Excellence Virtual, Instructor-Led Training (VILT) May 23rd – 24th, 2022 1:00 pm ET – 3:00 pm ET Duration: 2 Hours each day Register Now We’re excited to offer a Virtual Instructor-Led Center of Excellence event, which takes place May 23rd – 24th. Join these daily 2-hour sessions (from […]

ASC 842 Compliance: Paths of Lease Assistance Vaco

Webinar ASC 842 Compliance: Paths of Lease Assistance Thursday 25 February 2021 2:00pm ET | 1:00pm CT | 11:00am PT | Duration: 1 Hour CPE: 1 credit Presented by: Attendees will learn: Achieving compliance with limited resources (hint: not using spreadsheets!) Uncovering the challenges of the new accounting close Automating your monthly close reporting […]

ASC 842 Compliance: Paths of Lease Assistance

Leasing experts from Vaco and LeaseAccelerator cover how private organizations like yours can achieve ASC 842 compliance despite limited resources.

The ASC 842 Compliance Toolkit – LinkedIn Ads

The ASC 842 Compliance Tool Kit Are you gearing up for an ASC 842 compliance project in 2021? While many public companies are nearing the end of their adoption, private companies are just getting started. Get all the resources you need for a successful project with our 2021 Lease Accounting Survival Kit. Download these tried […]