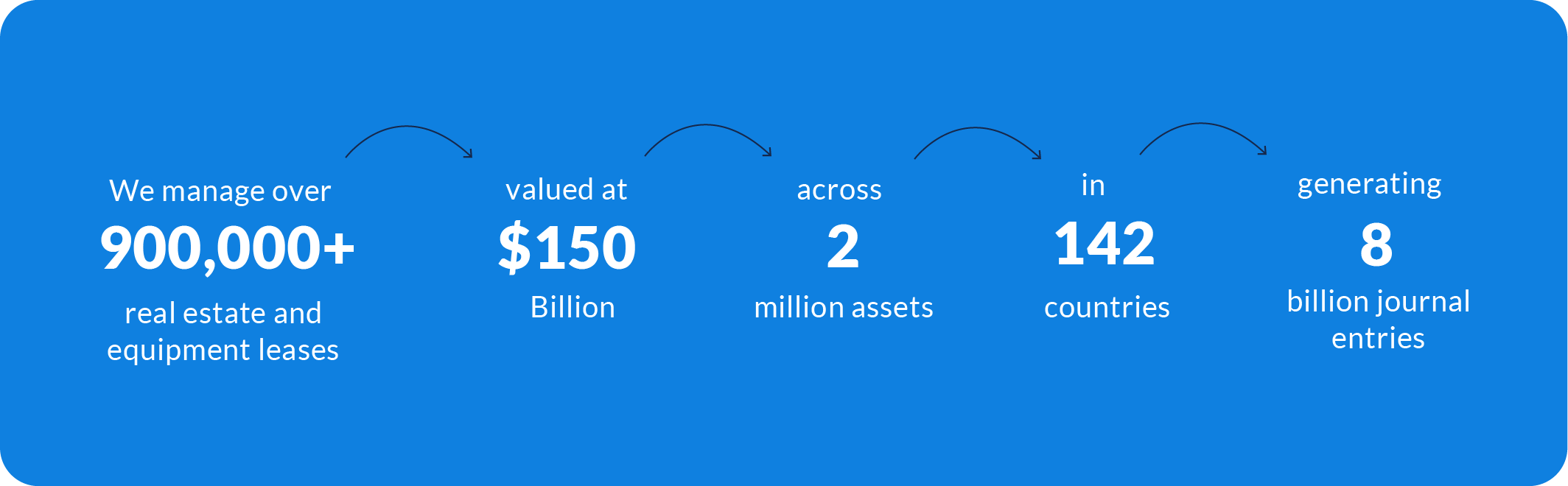

For over two decades, CFOs, Controllers, VPs of Real Estate, Treasurers, and Chief Procurement Officers have chosen LeaseAccelerator to transform leasing and lease management from a compliance project to a strategic initiative that generates cash flow and business insights.

Our clients are weathering market shifts – including changes in lease accounting and emissions standards, economic uncertainty, and pressure to consolidate strategic financial systems – with our end-to-end, asset-level, SaaS platform.

“LeaseAccelerator saves us thousands of hours per year.”

"LeaseAccelerator has the ability to handle our complex leases."

"LeaseAccelerator gives us greater visibility of our lease portfolio."

Overcoming leasing challenges

The drive to comply with lease accounting standards has been a powerful catalyst for long-overdue process automation. But now that finance teams have control over leased asset data, there are more opportunities for immediate savings and business improvement.

Here are a few common areas that LeaseAccelerator addresses:

Lease vs. Buy decisions aren’t consistent.

Lease financing isn’t sourced competitively.

Organizations struggle to track leased assets and spaces.

Equipment leases auto-renew, costing two to three times the original purchase cost.

Real estate teams miss critical renewal deadlines, resulting in higher rents.

All of these can be solved with LeaseAccelerator, the only unified lease accounting, lease administration, and lease lifecycle management platform available today.

No one is more passionate about real estate and equipment leasing than LeaseAccelerator. It’s the only thing we focus on, and the reason we were founded in 2003.

We’ve hired a dream team of lease and lease accounting experts from Global 500 companies, Big Four firms, and top ten lease financing companies. Our experts bring best practices in finance, accounting, treasury, tax, real estate, procurement, emissions, and supply chain functions to help drive your transformation.

LeaseAccelerator offers a platform for growth across the full lease lifecycle, with a starting point for every company, regardless of size and maturity. Our asset-level equipment and real estate lease accounting and administration applications deliver proven ROI and long-term compliance.